On this page · 8 sections

- Understanding Michigan's Corporate Tax Landscape

- Who Is Required to Pay Estimated Taxes?

- How to Calculate Your Estimated Tax Payments

- Michigan's Corporate Estimated Tax Deadlines for 2026

- Methods for Submitting Your Payments

- Navigating Penalties for Underpayment and Late Filing

- How Your Business Structure Affects Tax Obligations

- Adjusting Payments for Fluctuating Income

Understanding Michigan's Corporate Tax Landscape

For any founder operating in Michigan, navigating state tax obligations is a critical component of financial management. At the heart of this is the Michigan Corporate Income Tax (CIT), a 6.0% tax levied on the federal taxable income of C-corporations and other entities taxed as corporations, after certain state-specific adjustments. To ensure a steady flow of revenue and prevent businesses from facing a massive tax bill at year-end, the state requires companies to pay this tax in installments throughout the year. These are known as corporate estimated tax payments. Think of estimated taxes as a pay-as-you-go system for your business's income tax. Instead of settling your entire tax liability in one lump sum when you file your annual return, you estimate your total tax for the year and remit it to the Michigan Department of Treasury in four quarterly payments. This requirement is not optional. You might also find our guide on how to register an LLC in Michigan useful here. Any corporation that expects its total CIT liability for the tax year to exceed $800 must make these estimated payments. This threshold applies to most active businesses generating a profit in the state. It's important to distinguish the current CIT from the now-defunct Michigan Business Tax (MBT). While the MBT was largely replaced by the CIT in 2012, some businesses may still have lingering obligations or credits related to it. However, for nearly all founders launching a company today, the CIT is the primary corporate tax framework to understand. Mastering its requirements, from calculating your liability to meeting payment deadlines, is fundamental to maintaining good standing with the state and building a financially sound enterprise from day one.

Who Is Required to Pay Estimated Taxes?

The primary group obligated to pay Michigan corporate estimated taxes are C-corporations. If your business is structured as a C-corp and you anticipate owing more than $800 in Corporate Income Tax (CIT) for the year, you are required to make quarterly estimated payments. This applies to both domestic corporations formed in Michigan and foreign corporations that are doing business in the state and are subject to its tax laws. What about other common business structures, like S-corporations and Limited Liability Companies (LLCs)? The answer here is more nuanced and depends on their federal tax election. ## S-Corporations S-corps are generally considered 'pass-through' entities. This means the profits and losses are not taxed at the corporate level but are instead passed through to the individual shareholders, who then report this income on their personal tax returns. Consequently, S-corporations typically do not have a CIT liability in Michigan and are therefore not required to make corporate estimated tax payments. The tax obligation falls on the shareholders. This connects to our resource on LLC registration in Michigan, which covers the details. ## Limited Liability Companies (LLCs) By default, the IRS treats a single-member LLC as a 'disregarded entity' (taxed like a sole proprietorship) and a multi-member LLC as a partnership. In both of these default scenarios, the LLC is a pass-through entity, and the income is reported on the members' personal tax returns. Therefore, a standard LLC does not pay the Michigan CIT and does not make corporate estimated tax payments. However, an LLC has flexibility. It can file IRS Form 8832 to elect to be taxed as a C-corporation. If an LLC makes this election, it becomes subject to the Michigan CIT just like a traditional C-corp and must make estimated tax payments if its expected liability exceeds the $800 threshold. Similarly, an LLC can elect S-corp status, which would follow the pass-through rules described above.

How to Calculate Your Estimated Tax Payments

Accurately calculating your estimated tax payments is essential to avoid underpayment penalties. The process involves projecting your income for the entire year and determining your tax liability based on Michigan's 6.0% Corporate Income Tax (CIT) rate. There are two primary methods for this calculation. ## The Regular Installment Method This is the most straightforward approach. Your total required estimated payment for the year is the lesser of two amounts:

- 85% of your current year's total CIT liability. 2. 100% of your prior year's total CIT liability (this option is only available if the prior year was a full 12-month period and you had a tax liability). Once you determine this total amount, you simply divide it by four and pay that amount in each quarterly installment. For example, if your 2025 tax liability was $10,000, and you expect similar performance in 2026, you can use that as your base. For related guidance, see our article on forming an LLC in Michigan. Your total estimated payment for 2026 would be $10,000, paid in four installments of $2,500 each. This is known as the 'safe harbor' rule and protects you from underpayment penalties, even if your actual 2026 liability ends up being much higher. ## The Annualized Income Installment Method

This method is more complex but incredibly useful for businesses with fluctuating or seasonal income. Instead of estimating for the full year at the start, you calculate your income and tax liability at the end of each payment period. This allows your payments to rise and fall with your actual cash flow. You'll need to project your income and deductions for each quarter to determine the tax due for that period. This requires more diligent bookkeeping but prevents you from overpaying during slow months or underpaying after a period of rapid growth. If you use this method, you must use Michigan's Form 4914, Annualized Income Installment Worksheet for C Corporations, to document your calculations and file it with your annual return. For most new businesses without a prior tax year to reference, you must estimate your current year's income and pay at least 85% of the resulting tax liability to avoid penalties.

Michigan's Corporate Estimated Tax Deadlines for 2026

Meeting deadlines is non-negotiable when it comes to tax compliance. The Michigan Department of Treasury sets a firm schedule for quarterly estimated tax payments. For corporations that operate on a standard calendar year (January 1 - December 31), the due dates are consistent year after year.

The four quarterly payments for the 2026 tax year are due on the following dates:

- First Quarter (Jan 1 - Mar 31): Payment due April 15, 2026

- Second Quarter (Apr 1 - May 31): Payment due June 15, 2026

- Third Quarter (Jun 1 - Aug 31): Payment due September 15, 2026

- Fourth Quarter (Sep 1 - Dec 31): Payment due January 15, 2027

Note that the fourth quarter payment is due in January of the following year, before you file your annual return. It's crucial to mark these dates on your financial calendar. If a due date falls on a weekend or a state holiday, the payment is due on the next business day.

Fiscal-Year Filers

If your corporation operates on a fiscal year rather than a calendar year, your deadlines are adjusted accordingly. The payments are due on the 15th day of the fourth, sixth, ninth, and twelfth months of your fiscal year. For example, if your fiscal year begins on July 1, your first estimated payment would be due on October 15.

It is critical to understand that filing an extension for your annual corporate tax return (Form 4891, Michigan Corporate Income Tax Annual Return) does not grant you an extension to pay your estimated taxes. The extension only provides more time to file the final return paperwork. The tax liability itself must still be paid throughout the year according to the quarterly schedule. Missing these deadlines will result in the automatic calculation and assessment of penalties and interest, regardless of whether you have an extension to file.

Methods for Submitting Your Payments

The Michigan Department of Treasury offers several methods for submitting corporate estimated tax payments, with a strong preference for electronic transactions. For most businesses, electronic payment is not just a suggestion; it's a requirement.

Electronic Funds Transfer (EFT)

The most common and often mandatory method is Electronic Funds Transfer (EFT). You can make EFT payments directly through the Michigan Treasury Online (MTO) portal. MTO is a secure, free service that allows businesses to manage their state tax accounts, make payments, and view their filing history. To use it, you'll need to register your business on the MTO website. You can schedule payments in advance, ensuring you never miss a deadline. Payments can be made via EFT Debit (where the state pulls funds from your account) or EFT Credit (where you instruct your bank to send the funds).

Payment by Check

While electronic payment is preferred, it's still possible to pay by mail. To do this, you must complete Form 4913, CIT Estimated Tax for C Corporations. This voucher includes your business name, Employer Identification Number (EIN), and the tax year. You'll mail the completed voucher along with your check or money order to the address specified on the form. It's crucial to mail it well in advance of the deadline to ensure it's postmarked on time. Always write your EIN and the relevant tax year on the check itself to ensure proper credit.

As a founder, your focus should be on building your product and serving customers, not wrestling with state tax portals. While Lovie doesn't handle tax filings or payments directly, our platform is designed to streamline the foundational steps of your business. By using Lovie for formation and registered agent services, you get AI-driven compliance monitoring that sends reminders for critical state deadlines, helping you stay organized so you can focus on tasks like making timely tax payments through the proper channels.

Navigating Penalties for Underpayment and Late Filing

The Michigan Department of Treasury is strict about estimated tax requirements, and failing to comply can lead to significant financial penalties. These penalties are designed to encourage timely and accurate payments throughout the year. Understanding how they are calculated is key to avoiding them.

Penalty for Underpayment

If you fail to pay enough estimated tax, you will be subject to a penalty. The penalty is calculated at a rate of 25% per year (or 2.083% per month) on the amount of the underpayment for the period the underpayment existed. The underpayment is the difference between the amount you paid for a quarter and the amount you should have paid. This penalty is computed for each quarter separately. So, even if you overpay in a later quarter, it won't erase a penalty from an earlier quarter where you underpaid.

Interest Charges

In addition to the penalty, interest is charged on any tax that is not paid by the original due date of the annual return. The interest rate is variable and is set at 1% above the adjusted prime rate. Interest continues to accrue until the tax liability is paid in full.

Avoiding Penalties with 'Safe Harbor' Rules

The best way to avoid these charges is to meet one of the 'safe harbor' provisions. As mentioned earlier, you are generally protected from underpayment penalties if your total estimated payments for the year equal or exceed:

- 85% of your current year's total tax liability. This requires a reasonably accurate projection of your annual income.

- 100% of your prior year's total tax liability. This is often the safest and easiest option for established businesses with a stable income. To use this safe harbor, your business must have been in existence for the full 12 months of the prior tax year and have reported a tax liability for that year.

For new businesses in their first year of operation, the prior-year option isn't available. Therefore, you must make a good-faith effort to estimate your income and pay in at least 85% of your final tax bill to remain compliant. Diligent bookkeeping and conservative financial projections are a founder's best tools in this scenario.

How Your Business Structure Affects Tax Obligations

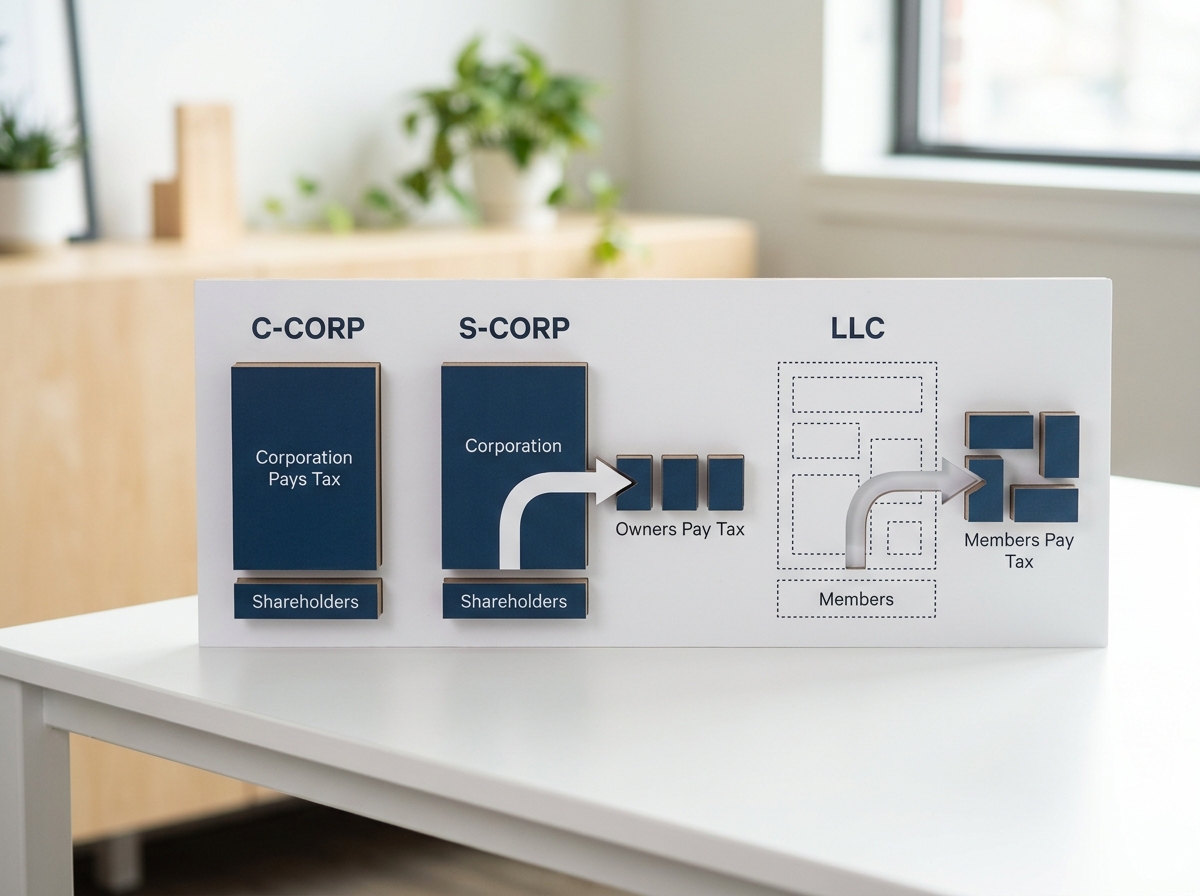

The business structure you choose when you form your company is one of the most consequential decisions a founder can make, with profound and lasting impacts on everything from liability to taxation. The requirements for Michigan corporate estimated taxes are a perfect example of this.

As we've established, the 6.0% Corporate Income Tax (CIT) and its associated estimated payment rules primarily target C-corporations. This structure creates a distinct legal and taxable entity separate from its owners. The corporation pays taxes on its profits, and then shareholders pay taxes again on any dividends they receive. This double taxation is a key consideration, but C-corps also offer benefits like the ability to issue stock, which is crucial for raising venture capital.

In contrast, S-corporations and default-taxed LLCs are pass-through entities. They don't pay entity-level income tax in Michigan. Instead, the profits 'pass through' to the owners' personal income, where they are taxed at individual income tax rates. This avoids double taxation and can be simpler for many small businesses. The owners themselves may need to make personal estimated tax payments to cover this income, but the business entity itself is generally off the hook for the CIT.

This is where the power of choice comes in. An LLC is a highly flexible structure. While it defaults to pass-through taxation, its members can elect for it to be treated as a C-corporation for tax purposes. Why would they do this? Perhaps they plan to seek venture funding, or maybe the corporate tax rate is more favorable for their income level and reinvestment strategy. Making this election fundamentally changes the LLC's obligations, subjecting it to the CIT and the quarterly estimated payment rules.

Choosing the right entity from the start is paramount. Lovie's AI-powered platform helps founders navigate these choices, providing clear information to assist in forming an LLC or C-Corp that aligns with their business goals. Lovie prepares and submits your formation documents, helping you establish the proper foundation so you can then work with tax professionals to manage specific obligations like estimated payments.

Adjusting Payments for Fluctuating Income

A startup's journey is rarely a straight line. Revenue can be unpredictable, with some quarters exceeding all expectations and others falling short. A rigid estimated tax plan based on initial projections may not serve a dynamic business well. If you pay too little, you risk penalties; pay too much, and you tie up precious working capital that could be used for growth. This is why Michigan's tax system allows you to adjust your estimated payments during the year.

If you realize your income for the year will be significantly different from your initial estimate, you should recalculate your total expected tax liability. This is especially important if you've been using the Regular Installment Method. Let's say you projected a $20,000 annual tax liability and have been paying $5,000 per quarter. After a blockbuster second quarter, you now project your total liability will be $40,000. To avoid an underpayment penalty, you must adjust your remaining payments.

Here’s how to adjust:

- Recalculate your total estimated tax for the year. In our example, it's now $40,000.

- Determine the total amount that should have been paid to date. By the end of the second quarter (June 15 deadline), you should have paid 50% of your total estimated tax, or $20,000.

- Subtract what you've already paid. You paid $5,000 for Q1 and $5,000 for Q2, for a total of $10,000.

- Make up the shortfall. You have a $10,000 shortfall ($20,000 required - $10,000 paid). You should add this shortfall to your next estimated payment. Your Q3 payment would be your regular installment ($10,000) plus the shortfall ($10,000), for a total of $20,000.

This same logic applies if your income is lower than expected. You can reduce later payments to avoid a large refund at the end of the year. For businesses experiencing this kind of volatility, the Annualized Income Installment Method is often a better fit from the start, as it builds these adjustments into its core calculation process.

Frequently asked questions

Do LLCs pay corporate estimated taxes in Michigan?

Generally, no. By default, LLCs are treated as pass-through entities for tax purposes. This means the income 'passes through' to the members, who pay personal income tax on it. However, if an LLC formally elects to be taxed as a C-corporation with the IRS, it then becomes subject to the Michigan Corporate Income Tax (CIT) and must make estimated payments if its expected tax liability exceeds $800.

What is the Michigan CIT rate for 2026?

The Michigan Corporate Income Tax (CIT) rate is set by state law. As of the latest information, the rate is a flat 6.0%. Tax rates can change based on legislative action, but this rate has been stable for several years. You should always verify the current rate with the Michigan Department of Treasury when calculating your payments.

How do I pay Michigan corporate taxes if I'm a new business with no prior year income?

As a new business, you cannot use the '100% of prior year's tax' safe harbor rule. Instead, you must make a good-faith estimate of your net income for your first year of operation. Calculate your expected tax liability based on this projection. To avoid penalties, your total estimated payments must amount to at least 85% of the tax you ultimately owe on your first annual CIT return.

Can I get an extension to pay my estimated taxes in Michigan?

No. An extension to file your annual tax return does not grant an extension to pay your tax liability. The quarterly estimated tax payments have firm due dates, and you must remit payment by those deadlines to avoid penalties and interest, even if you have an extension to file your final return.

What is the difference between the Michigan Business Tax (MBT) and the Corporate Income Tax (CIT)?

The Michigan Business Tax (MBT) was a broader tax that included both a modified gross receipts tax and a business income tax. It was repealed and replaced by the 6.0% Corporate Income Tax (CIT) in 2012. The CIT is a much simpler tax levied only on the net income of C-corporations and entities that elect to be taxed as such. While most businesses no longer deal with the MBT, some may have carryover credits or other lingering issues from that system.

What happens if I overpay my Michigan estimated taxes?

If your total estimated payments for the year exceed your final tax liability, you will have an overpayment. When you file your annual Michigan CIT return (Form 4891), you can choose how to handle this overpayment. You can either request a full refund from the state or apply all or part of the overpayment as a credit toward the next year's estimated tax payments.

Are federal estimated tax rules the same as Michigan's?

While the concepts are similar, the rules, rates, and forms are different. The federal government has its own set of deadlines and calculation methods for corporate estimated taxes, which are paid to the IRS. Michigan's rules apply only to your state tax liability. You must manage and pay your federal and state estimated taxes separately.

Michigan Formation Data Insights

| State Filing Fee | $50 |

| Annual Fee | $25 |

| First Year Total | $75 |

| Processing Time | 8.4 days avg (official: 7-10 days) |

| Corporate Tax Rate | 6% |

Key Insights

- Michigan'de LLC kurulum maliyeti ulusal ortalamanın $149 altında — toplam ilk yıl maliyeti $75.

- Lovie platformu üzerinden Michigan LLC başvuruları ortalama 8.4 iş gününde onaylanmaktadır (eyalet resmi süresi: 7-10 gün).

- Michigan merkezli işletmeler için EIN onay süresi ortalama 4.0 gündür.

- Michigan kurumlar vergisi oranı %6.0'dir (ulusal ortalama: %6.57).

Financial Services — Formation Context

Recommended Entity: LLC or C-Corp

Key Tax Benefit: Professional development, licensing fees

Compliance Priority: SEC/FINRA registration, state money transmitter licenses

Data sources: State Secretary of State offices, IRS, Tax Foundation (2026). Platform metrics based on anonymized Lovie user data.

Key Concepts: Business Formation

US Business Formation guides entrepreneurs through the business formation process with actionable steps. Key components include LLC formation, entity registration, and state filing, each playing a critical role in the business formation process. Understanding liability protection and tax optimization is essential, as these factors directly impact legal compliance.

When evaluating business formation options, factors such as business entity types and formation process should inform your decision-making process.

Entity Relationships

- Business Formation requires LLC formation

- Business Formation includes entity registration

- Business Formation establishes state filing

- Business Formation defines business structure selection

Quick answers

What do I need to know about Mass Corporations Search for my business?

Understanding Mass Corporations Search is essential for business compliance and operational success. The specific requirements vary by state and industry.

How does Mass Corporations Search affect my business formation?

This aspect of business formation directly impacts your legal standing, tax obligations, and operational flexibility.

Explore Formation Guides

State-specific formation guides, cost breakdowns, compliance checklists, and expert comparisons — updated for 2026.

Popular Guides

LLC Formation Guides

- How to Form an LLC for AI ML Iowa (2026) | Lovie

- How to Form an LLC for Construction Mississippi

- How to Form an LLC for Telehealth California (2026) | Lovie

- How to Form an LLC for Accounting in Utah

Lovie is not a government agency, law firm, or professional advisory organization. Lovie is a private business-formation service that prepares and submits filings to the appropriate state agencies on your behalf — we do not issue government documents, and state approval times are not controlled by Lovie. Information on this page is general and not legal, tax, or financial advice.